Category: Venture Capital & Term Sheets

-

Venture Capital Term Sheet Survival Guide

If you are a founder with a venture capital term sheet in your inbox, you’re not “almost closed.” You’re at the moment where a few pages of business terms quietly lock in years of economics and control for your startup. A VC term sheet is a short summary of the key terms of a proposed…

-

Founder Secondary: Liquidity and Signaling

TL;DR: A Founder Secondary is when you sell some of your shares for cash usually in connection with a financing. It’s typically healthy when it’s modest, the round is otherwise strong, and it reduces personal financial pressure so you can stay focused; it’s usually dangerous when it’s large, early, or a major negotiation point, because…

-

Protective Provisions: Congratulations, You Need Permission

If you’re negotiating a venture financing, “protective provisions” are the investor veto rights that quietly move real control away from the boardroom and into the preferred stockholder class. The short version: once you sign them, you can’t do a bunch of very normal startup things (raise money, sell the company, change the option pool, even sometimes…

-

Information Rights: Reporting Creep and the “CFO-by-Investor” Trap

If you’re signing a term sheet (or closing a round) and the information rights feel like “just boilerplate,” pause. The short answer: you should agree to a reporting cadence you can reliably hit without turning your CEO (or CFO or finance lead) into an on-demand analyst for a single investor. Most information rights are meant…

-

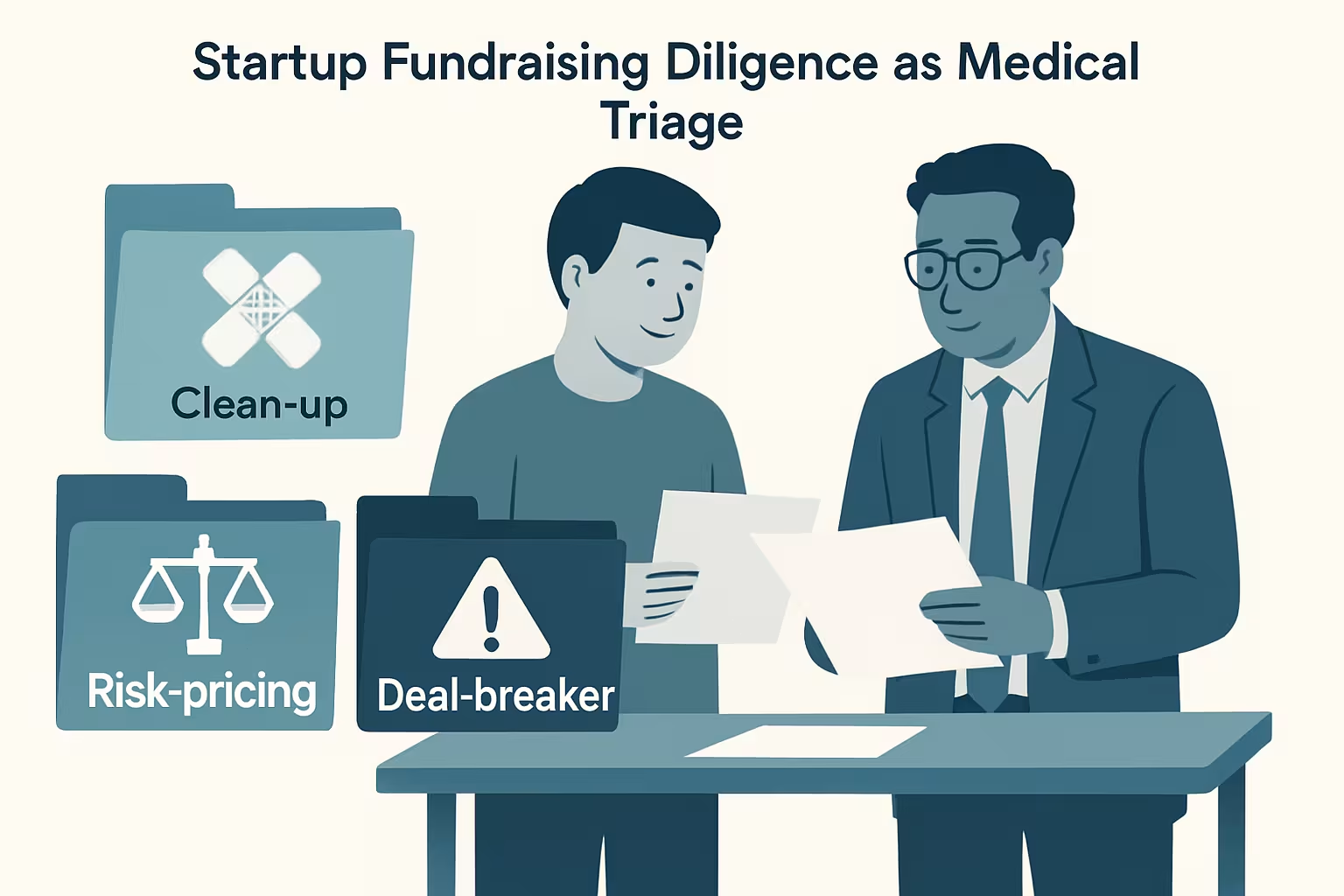

The Difference Between a Diligence Issue and a Deal‑Breaker in Venture Financings

If you’re raising a seed or Series A round, here’s the short answer: most diligence issues are fixable, but a small few will make an investor walk, either because they create uncapped downside, uncertainty about ownership, or a cleanup job that will outlast the deal momentum. The hard part isn’t spotting “a problem.” It’s sizing…

-

Pay-to-Play: The “Fairness” Term That’s Really a Squeeze

If you’re a founder facing a “pay-to-play” in a down round or a messy inside recap, here’s the short answer: it’s usually a leverage tool that gets sold as a fairness principle. Sometimes it’s a reasonable way to make sure investors who want the upside also share the pain. Other times it’s a pressure tactic…

-

A “Clean Cap Table” Doesn’t Mean What You Think

If you’re fundraising and someone tells you to “clean up your cap table,” they usually don’t mean “have fewer stockholders.” They mean: make your ownership record reliable, documentable, and free of surprises. That means no missing signatures, no mystery SAFEs, no side letters you forgot about, and no equity you can’t actually prove. This matters…

-

When to Say No to Investment Money

If you’re raising money for a startup, the short answer is this: you should say no when the capital comes with terms, timelines, or people that predictably and materially reduce your options to build, to raise the next round, or to sell the company later. You’ll hear some version of “lawyers kill deals” any time a…

-

Venture Capital Bridge Extension Round Structures

Thinking about all the potential bridge extension rounds that will need to be closed in late 2024 and 2025, and here are my thoughts on the structure: If you do equity, and assuming it’s the same valuation, you could do an ‘extension round’ which essentially builds off the prior preferred round. This would increase the…

-

U.S. VC Process for Indian Startups

As a startup in India, closing on U.S. venture capital is similar to doing so if your company was completely US-based, with a few notable differences. I’ve represented several India-based startups through venture capital financings. To name just a few, clients have included Freshworks (formerly FreshDesk), WizRocket, and Shopalyst. They, along with other clients, have…