Author: Ryan Roberts

-

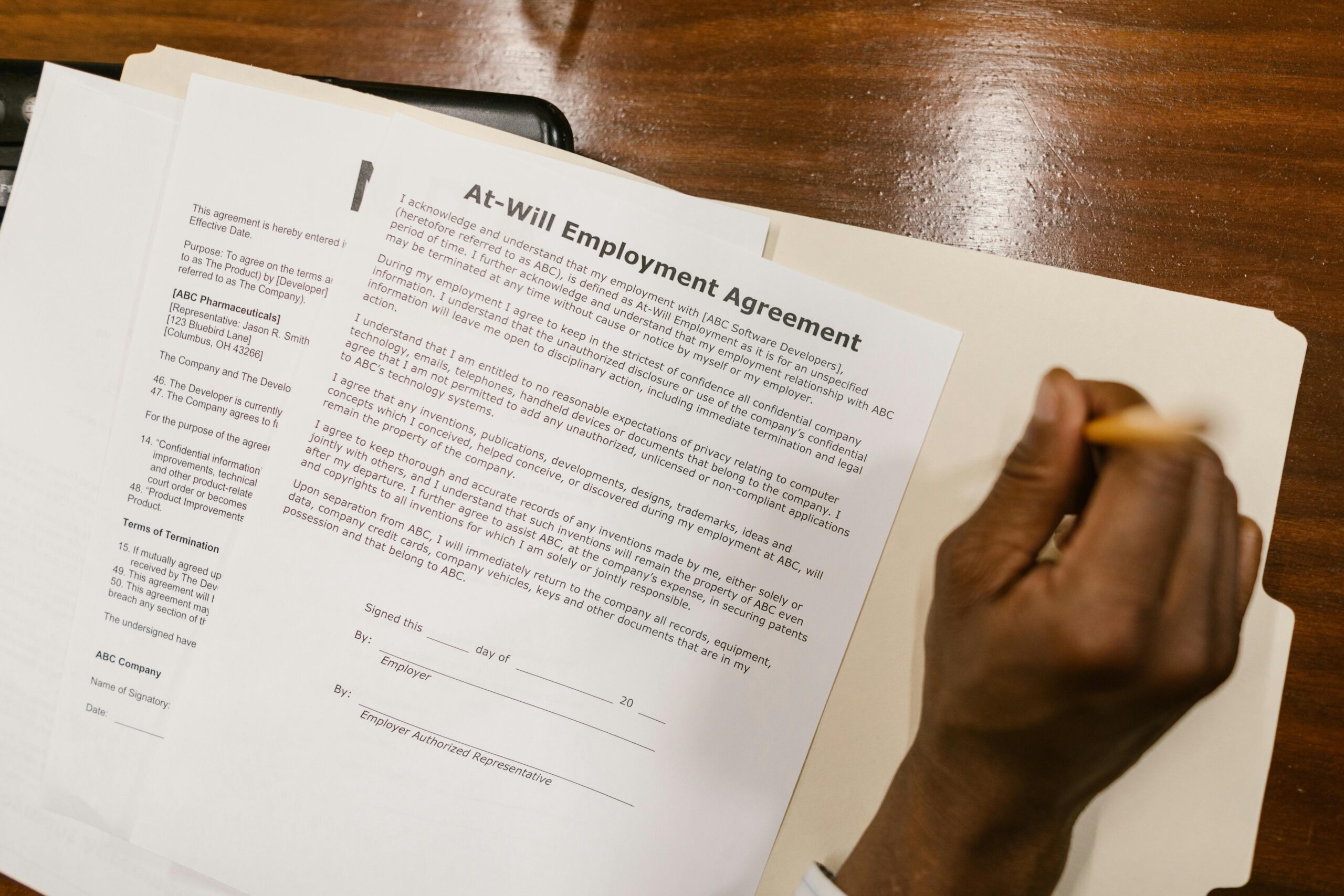

Founder Employment Agreements in Exits

TL;DR: In most acquisitions, founder employment agreements is where the buyer sets your post-close reality: role, reporting line, compensation and retention, severance, and the exit ramps if it does not work out. Buyers often deliver a broad, standard-form restrictive covenant package late in the process to create time pressure, and it can include a much…

-

Founder Secondary: Liquidity and Signaling

TL;DR: A Founder Secondary is when you sell some of your shares for cash usually in connection with a financing. It’s typically healthy when it’s modest, the round is otherwise strong, and it reduces personal financial pressure so you can stay focused; it’s usually dangerous when it’s large, early, or a major negotiation point, because…

-

The Ultimate Pre-Incorporation Checklist

TL;DR: If your startup is pre-incorporation, you can still lock down the things that usually blow up later: who owns what, who can bind the company, and whether your IP is actually yours. The expensive problems aren’t abstract legal issues. They’re diligence surprises like a cofounder who “thought” they owned 50%, contractor code with unclear…

-

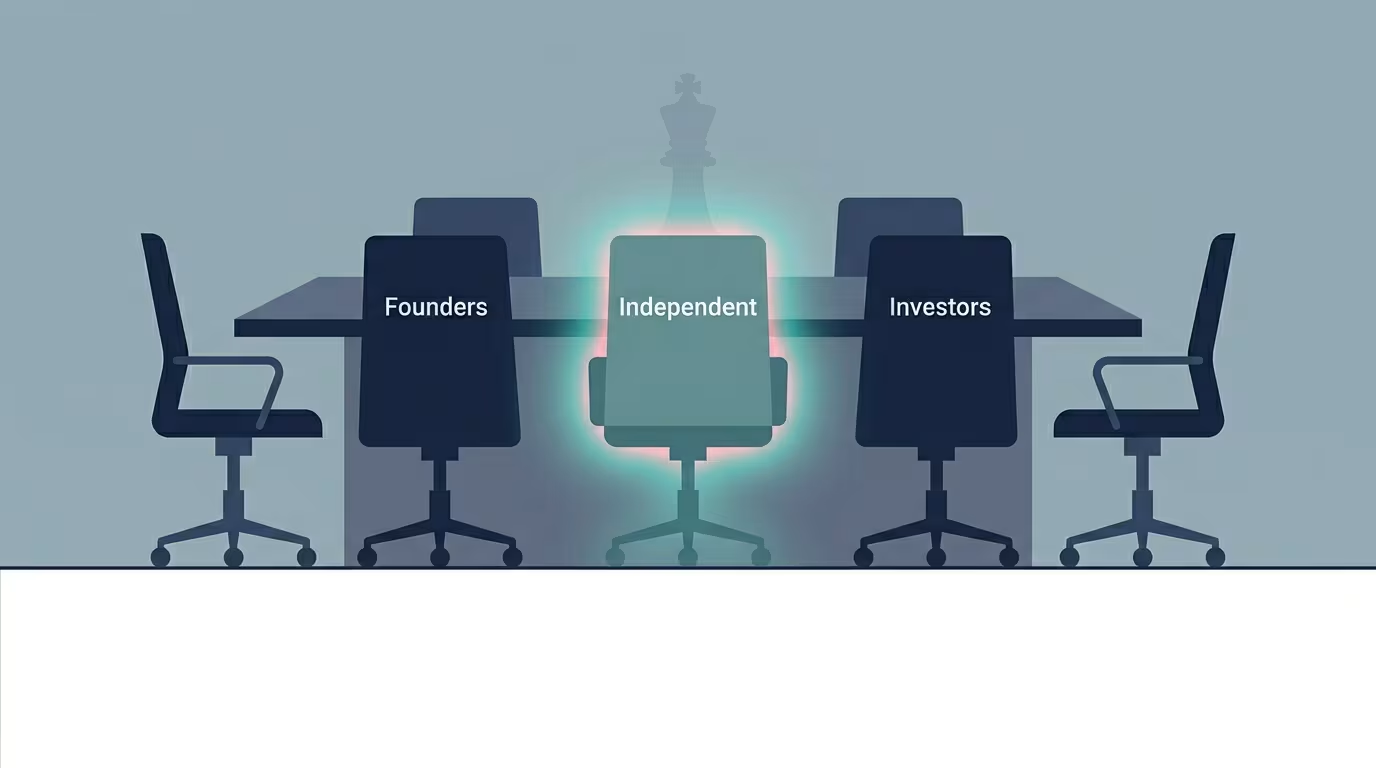

Board Composition: Sticky Control Shifts

If you’re raising a priced round (especially Series A), board composition is one of the few terms that can change your day-to-day reality as a CEO faster than your cap table does. Once you give up voting control at the board level, you may not be able to “earn it back” later without someone else’s…

-

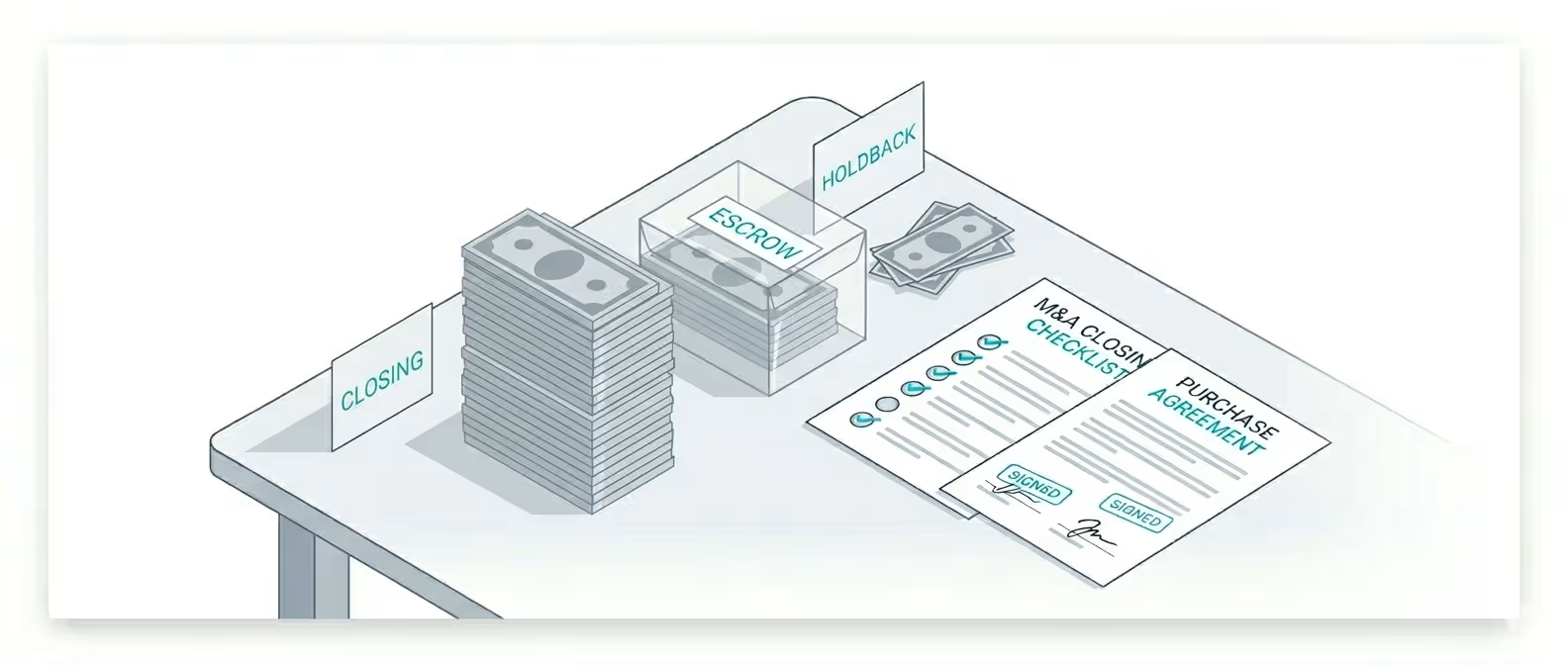

Escrow and Holdback in Startup M&A

TL;DR: In most private-company startup acquisitions, it’s normal for the buyer to hold back a portion of the purchase price in an escrow (or as a holdback) for 12 to 18 months to cover post-closing surprises, so the real question is not “why isn’t my money here,” but how big it is, how long it lasts, and how easy it is for…

-

Venture Studio Taking 50% Equity for $0: Half Your Company for Promises

tl;dr: “50% for $0” is usually a brutal trade: you’re handing over permanent ownership to a venture studio for promised introductions + some operating help…often while the studio’s equity doesn’t vest. If they’re truly acting like co-founders, make them earn it via vesting/milestones. Otherwise, walk. They are trying to make you glorified employees. If you’re…

-

Protective Provisions: Congratulations, You Need Permission

If you’re negotiating a venture financing, “protective provisions” are the investor veto rights that quietly move real control away from the boardroom and into the preferred stockholder class. The short version: once you sign them, you can’t do a bunch of very normal startup things (raise money, sell the company, change the option pool, even sometimes…

-

Information Rights: Reporting Creep and the “CFO-by-Investor” Trap

If you’re signing a term sheet (or closing a round) and the information rights feel like “just boilerplate,” pause. The short answer: you should agree to a reporting cadence you can reliably hit without turning your CEO (or CFO or finance lead) into an on-demand analyst for a single investor. Most information rights are meant…

-

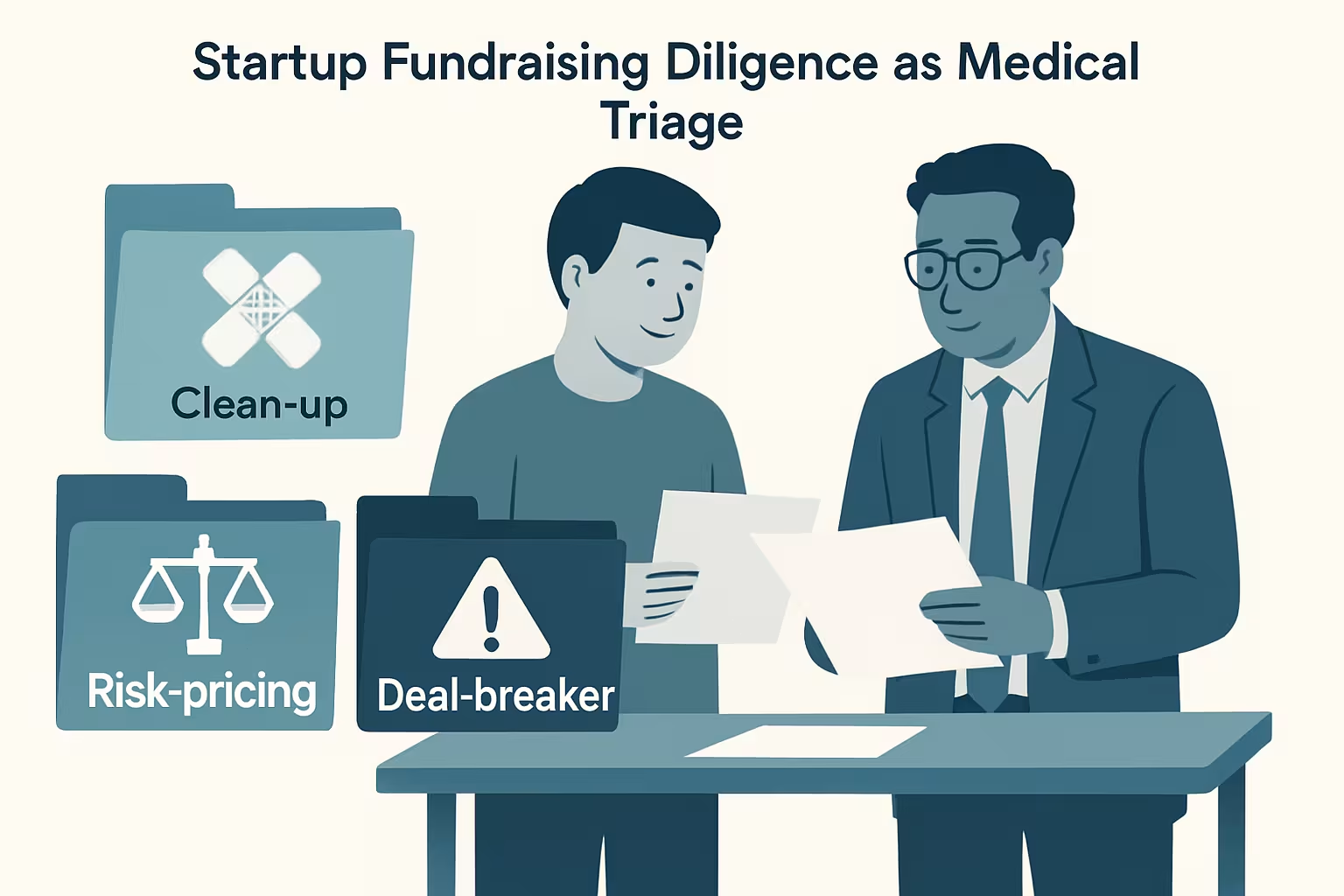

The Difference Between a Diligence Issue and a Deal‑Breaker in Venture Financings

If you’re raising a seed or Series A round, here’s the short answer: most diligence issues are fixable, but a small few will make an investor walk, either because they create uncapped downside, uncertainty about ownership, or a cleanup job that will outlast the deal momentum. The hard part isn’t spotting “a problem.” It’s sizing…

-

Online Cap Tables: Great Tools, Real Limits

If you’re looking at online cap tables like Carta, Pulley, Morgan Stanley’s Shareworks, or Fidelity’s Private Shares, the short answer is: they’re a helpful secondary record and workflow tool, not the actual “truth” of your capitalization. They can be great for issuing and tracking equity, running option exercises, generating certificates, and modeling financings. But the platform’s outputs…